Last modified by: Alpine Crew -

How to Read the PIER Report

If you are wanting to create a PIER review outside of the T4 preparation process - see Creating a PIER Review.

Here's how to read the PIER report:

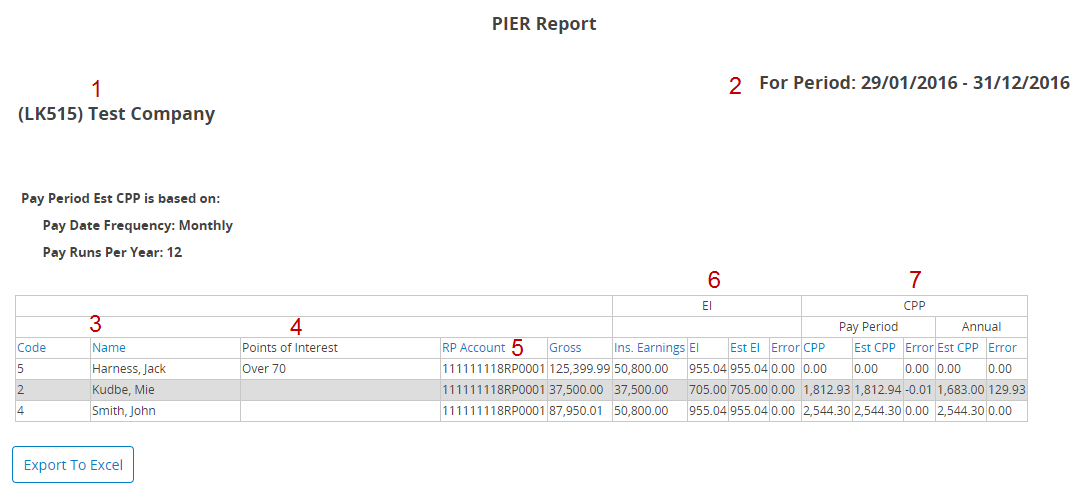

1. Company Information

On the top left, the header contains the company name and the payroll frequency details. The payroll frequency is used to calculate the per pay period exemption for the Pay Period Estimated CPP.

2. Date Range

Located at the top right of the header, the Date Range identifies the dates where data reported is coming from.

3. Employee Demographics

The first two columns of the table show the Employee Code and Employee Name. By default, the report loads in alphabetically order based on the Employee Name.

Hint: To easily sort through any of the table data, you can click the Column Name to sort the table in ascending or descending order based on that column.

4. Points of Interest

This column indicates any exemptions that are set in the system. It also identifies events such as an employee turning 18 or 70. This information is key in helping determine why an error may be present in the employee's CPP or EI contribution.

5. RP Account

This column indicates which RP account the employee belongs to.

Note that there are separate screens for T4 preparation for multiple RPs, but all RP accounts will appear in the PIER report created.

6. Employment Insurance (EI)

The Employment Insurance sections shows:

Insurable Earnings (Ins. Earnings) = the employees insurable earnings to date.

The Insurable Earnings column may not always equal the Gross pay depending on if there are non-insurable earnings, insurable benefits or if the employee became EI exempt at some point in the year.

Employment Insurance (EI) = the amount of EI deducted from the employee to date.

Estimated Employment Insurance (Est EI) = the PIER's calculated EI contribution for the employee to date, based on the reported Insurable Earnings.

Error = the difference between the EI and the Est EI. If there have been no adjustments to the payroll calculations throughout the year, the error reported here should be 0.00 (give or take a penny due to rounding).

For Errors that do not equal 0, take note of the negative amounts. A negative error means that the employee is deficient or has contributed less than what CRA expects. If left uncorrected, this may result in the company receiving a PIER from CRA. (See note on Error Threshold below.)

Prior to Year End, recovering EI deficiencies can be done via adjustments on the next pay run or an Ad Hoc run. Please contact Alpine Crew if you require assistance in making adjustments. Call 1-800-335-0039 or email alpinecrew@ibexpayroll.ca

7. Canada Pension Plan (CPP)

The Canada Pension Plan calculations are divided into 2 sections.

The Pay Period section looks at CPP contributions for the number of pay periods completed in the date range selected. It is a good measure to see if you have deducted the correct amount of CPP for the wages paid out so far. It includes:

Canada Pension Plan (CPP) = the amount of CPP deducted from the employee to date.

Estimated CPP (EstCPP) = the PIER's calculated CPP contribution for the employee to date. This calculations is based on the exemption for the number of completed pay runs included and not the annual CPP exemption.

Estimated CPP = CPP Rate x (Pensionable Earnings - (Annual Exemption / Pay Runs per Year x # of Completed Pay Runs))

Error = the difference between the CPP and the EstCPP for the pay runs included in the date range.

The Annual section looks at CPP contributions as if the year has ended, and all wages have been paid out. When running the PIER at Year End, this is the section you want to pay attention to. It includes:

Estimated CPP (EstCPP) = the PIER's calculated CPP contribution for the employee to date. This calculation is based on the annual exemption regardless of the number of pay runs completed.

Estimated CPP = CPP Rate x (Pensionable Earnings - Annual Exemption)

Error = the difference between the CPP (first column in CPP section) and the EstCPP for the year. If there have been no adjustments to the payroll calculations throughout the year, the error reported here should be 0.00 (give or take a penny due to rounding).

For Errors that do not equal 0, take note of the negative amounts. A negative error means that the employee is deficient or has contributed less than what CRA expects. If left uncorrected, this may result in the company receiving a PIER from CRA. (See note on Error Threshold below.)

Prior to Year End, recovering CPP deficiencies can be done via adjustments on the next pay run or an Ad Hoc run. Please contact Alpine Crew if you require assistance in making adjustments. Call 1-800-335-0039 or email alpinecrew@ibexpayroll.ca

Note: Error Threshold

If the total adjustments for the entire RP account will result in a balance owing or a credit of $2 or less on the T4/T4A summary, including both employee and employer portion, CRA will not charge or refund this difference.